Mortgage Rates Today: The Latest 'Drops,' 30-Year Hype, & Refinance Reality

Mortgage Rates Just Hit Their Lowest Point This Year: Is This Really the "Good News" They're Selling You?

Alright, folks, buckle up. The headlines are screaming, practically doing cartwheels: "Mortgage rates just hit their lowest point this year!" "Lowest 30-year rate this year!" Sounds great, right? Like a warm blanket on a cold November night. But if you’re anything like me—and I’m guessing you are, since you’re here instead of reading some corporate mouthpiece—you’re probably squinting at that "good news" with a healthy dose of suspicion. Because let’s be real, "lowest this year" ain't exactly "lowest ever." It’s more like saying your car’s check engine light is only flickering today, instead of being a solid, terrifying beacon of impending doom. What a joke.

I mean, seriously, are we supposed to pop champagne because the average 30-year fixed rate for a purchase tied its lowest point of 2025 at 6.06%? Or because on November 27th, it dipped to a crisp 6.00% according to some reports? Give me a break. This whole "drop" is barely a ripple. No, wait, it's more like a drip in a desert when you're dying of thirst. A single drop of water, and they expect us to believe the drought is over? Please. I remember when rates were in the 2s and 3s. That was good news. This? This is just less bad news, and even that’s debatable depending on which day of the week you check. It's enough to make you wanna throw your phone across the room, watching these numbers dance around like a bad TikTok trend.

The Numbers Game and the Fed's Shell Game

Let’s dive into the glorious specifics they’re so eager to parade. We’re talking 6.06% for a 30-year fixed purchase on November 25th, maybe even 6.00% by the 27th, if you believe all the sources. Mortgage Rates Drop Before Thanksgiving | Today, November 26, 2025 Refinance rates? Higher, naturally. Always higher. 6.20% for a 30-year refi on the 25th, dipping to 6.14% by the 27th. And the 15-year fixed, the one that makes your monthly payment a gut punch but saves you a fortune in the long run? That’s sitting around 5.50-5.53%. Better, sure. But remember that $400,000 mortgage example? At 6.06% over 30 years, you're still handing over nearly $470,000 in interest alone. That's almost another house, just for the privilege of borrowing money.

And who’s pulling the strings on this puppet show? Oh, just our good friends at the Federal Reserve. They cut rates in September and October. They’re "considering" another cut in December, with the CME FedWatch tool predicting an 85% chance of another quarter-point slice. Eighty-five percent! Sounds pretty confident, right? But then you read the fine print, and economists "don't expect drastic mortgage rate drops before the end of 2025." And for 2026? "Might ease a bit lower." Might. Might. It's like they're dangling a carrot on a string, just out of reach, forever. They talk about "uncertainty" and "volatility," which is just a fancy way of saying, "We don't really know what the heck we're doing, but we'll sound smart while we don't do it."

I’m telling you, it’s a classic bait-and-switch. They get everyone hyped about these tiny dips, hoping you’ll jump in, lock a rate, and then… well, then you're locked in. Meanwhile, the Fed's balance sheet is shrinking, which tends to push rates up. So while they're making a show of cutting the federal funds rate, there are other levers at play that are quietly working against you. It's a financial hydra, cut off one head, and another pops up. They want you to focus on the shiny new rate while the underlying system keeps us all on a treadmill. And offcourse, the "experts" at Fannie Mae and MBA have forecasts for 2026 that are all over the map, from 5.9% to 6.4%. So much for certainty, eh? It’s almost as if they’re just making it up as they go along.

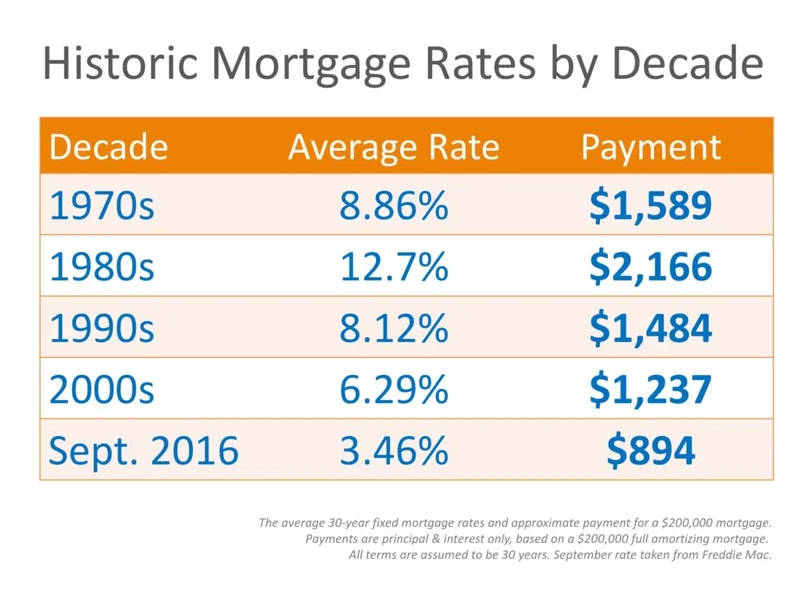

Then there’s the sheer audacity of telling us that 7% rates aren’t "unusually high" historically. They pull out charts from the 70s and 80s, where rates hit 18%, to make us feel better about 6%. That's like telling someone who just got a flat tire, "Hey, at least your car didn't explode like that one time!" It's a deflection, pure and simple. We're living in a different economy, with different wages, different cost of living. Comparing apples to mangos from forty years ago is just insulting. And don’t even get me started on the "golden handcuffs"—all those poor souls who bought homes when rates were 2-3% and now can’t move because they’d be trading a golden ticket for a lump of coal. It's a mess. A beautiful, complicated, rigged mess.

The Illusion of Choice and the Waiting Game

So, what’s a hopeful homebuyer or a desperate refi-seeker supposed to do? They tell you to get your credit score sky-high, keep your debt-to-income ratio pristine, and shop around with multiple lenders. Which, fine, that's just common sense, right? But it’s presented like some secret handshake to unlock the "best" rate, when the "best" rate right now is still a far cry from genuinely affordable for many. It’s like being told to climb Mount Everest to get a glass of water, when what you really need is a functioning municipal water supply.

This whole thing feels like a waiting game, a prolonged tease. Will rates drop more before the end of the year? Maybe. Will they ease slightly in 2026? Perhaps. But the underlying message from the "experts" is clear: don't hold your breath for those sweet, sweet sub-4% rates again. They were a blip, a "pandemic-induced economic slump" anomaly, never to be seen again in our lifetimes. Or maybe I'm just too jaded, who knows. But when every piece of "good news" comes with a dozen caveats and conflicting forecasts, it’s hard not to feel like you’re being played.

You’re left trying to decipher tea leaves, watching the stock market, Treasury yields, oil prices, and even the CNN Fear & Greed Index, all supposedly giving clues about where mortgage rates are headed. But then they admit, "Before the pandemic... you could look at the above figures and make a pretty good guess... But that’s no longer the case." So, they give us all this data, then tell us it’s basically useless. Fantastic. Just what we needed—more ambiguity in an already opaque market.