Mortgage Rates Today: The Latest on 30-Year & Refinance Rates, and What it Means for Your Future

The Great Unlocking: Why November's Mortgage Rate Dip is More Than Just Numbers

Alright, let's talk about something truly fascinating, something that’s been a silent, stubborn wall for far too long, and that’s finally starting to show some cracks: mortgage interest rates. For what feels like an eternity, we've watched these numbers hover, making homeownership or even a sensible refinance feel like a distant dream, a relic of a bygone era. But if you’ve been paying attention to the latest data, especially from NerdWallet and Zillow, you’ll know that something is shifting. And honestly, when I first saw the trends for late November 2025, I found myself leaning forward in my chair, a genuine spark of excitement igniting. This isn't just a blip; it's a signal.

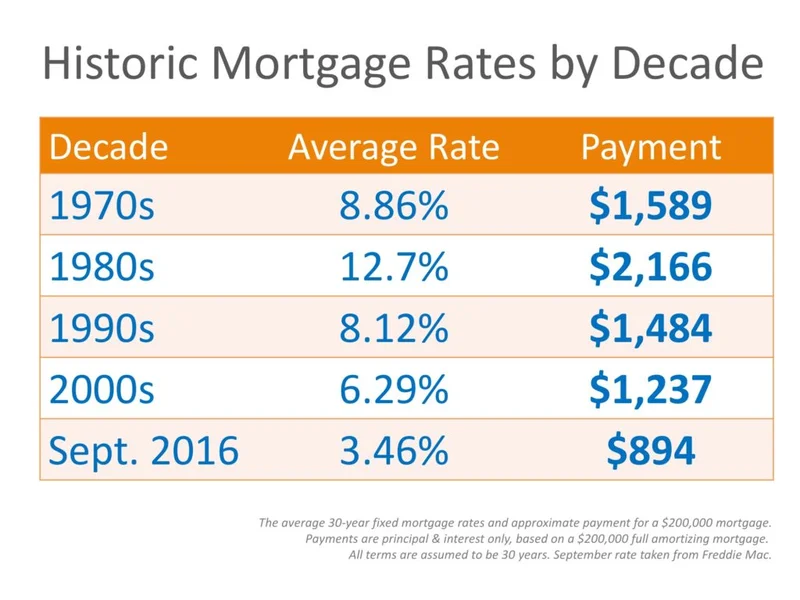

Remember how just a few months ago, the idea of a 30-year fixed-rate mortgage below 6% felt like pure fantasy? We were stuck in this gravitational pull of 7% and higher, a real drag on the collective ambition of millions. But here we are, staring down average 30-year fixed rates that dropped two basis points to 6.03% APR on November 27th, and even a Zillow average hitting 5.99% on the 26th. And 15-year fixed rates? Down to 5.46% APR. Even 5-year ARMs are seeing a dip to 6.64% APR. These aren't just minor adjustments; they represent a significant, tangible easing, a collective exhale for anyone who’s been on the sidelines. It's like the market is finally taking a deep breath after holding it for far too long, and for homeowners with rates around 7%, this is a genuine refinance opportunity knocking.

The Economic Tides Are Turning: A New Chapter Begins

What’s driving this rather dramatic, yet quietly profound, shift? It’s a confluence of factors, a fascinating interplay between macroeconomics and human expectation. The chatter around a potential Federal Reserve rate cut in December has gone from whisper to a full-blown roar. When New York Fed president John Williams, San Francisco Federal Reserve president Mary Daly, and Federal Reserve Governor Christopher Waller all start signaling support for a cut, you know it’s not just speculation anymore. Traders are now seeing an 83% chance of a 25-basis point cut at the Fed’s December 9-10 meeting. That’s a near certainty in the volatile world of finance, and it’s already being "priced in" by lenders. According to Realtor.com, Mortgage Interest Rates Dip to 6.23% as Split Fed Signals Another Cut.

This isn't just about the Fed's direct actions on short-term rates, mind you. It's about the broader perception of the U.S. economy. The labor market, while still robust in many areas, is showing signs of weakening, with job losses at private employers speeding up. This cooling effect gives the Fed more room to maneuver, more reason to step in and provide a cushion. Think of it like a giant, complex engine that’s been running too hot, and now the mechanics are finally seeing a chance to dial down the thermostat without stalling the whole operation. This delicate dance between inflation, employment, and monetary policy is what sets the stage for our mortgage rates, and right now, the dance is leaning towards lower borrowing costs. What an incredible moment to witness!

Beyond the Numbers: Reclaiming the Future You Envisioned

So, what does this actually mean for you, for us, for anyone who’s dreamt of a new home or a more manageable monthly payment? It means empowerment. For months, we've heard the lament of "rates are too high," a sentiment that has pushed hundreds of thousands of potential buyers and refinancers to the sidelines. Freddie Mac research tells us that comparing even a few lenders could save you $600 to $1200 annually, but when rates were sky-high, even those savings felt like rearranging deck chairs on the Titanic. Now, with a quarter-point drop potentially saving you $22,000 over the life of a $360,000 loan, those fractions of a percentage point suddenly become monumental.

This is the "Big Idea" I want us all to grasp: the market is finally beginning to unlock the potential that's been trapped. It's not just about cheaper money; it's about renewed access to a fundamental aspiration – a place to call your own, a chance to invest in your future, a path to financial stability. We're seeing contract signings jump, purchase applications rise, and a palpable shift in the collective mood. This isn't just a financial transaction; it's a re-opening of possibilities. Of course, with great opportunity comes great responsibility. We must approach these shifts with financial literacy, comparing loan estimates, understanding APR versus interest rate, and ensuring we're not overextending ourselves just because the door is finally ajar. But what an incredible feeling to finally see that door opening, isn't it?

The Horizon Is Bright

This isn't just a momentary dip; it's a potential turning point. The sustained pressure from the Fed, coupled with a cooling labor market, points to a continued easing of mortgage rates as 2025 draws to a close and we step into 2026. This isn't just about numbers on a screen; it's about the ripple effect on countless lives, the unlocking of dreams deferred. We're witnessing the start of a new chapter where the market, finally, is working with us, not against us. It's a reminder that even in complex systems, the human drive for progress and stability can find its way through. And that, my friends, is a truly inspiring sight.